Unusual Week Ahead

June 29th

What’s up everyone,

Welcome back. We are standing at the door of the second half of 2026, and I want you to take a second and appreciate where we just came from. The first half handed us a hot war in Iran, a ceasefire that nobody fully trusts yet, an OpenAI IPO saga, a SaaS repricing that wiped trillions off software, and an AI trade that has gone from “buy everything” to “okay, but at what price.” And through all of that, the indices are still parked near record territory. That tells you something about this tape that I keep coming back to: it does not want to break. It wants to rotate.

Last week was the cleanest example of that we have seen all year. Tech got taken to the woodshed while the rest of the market shrugged and kept grinding higher. And then Monday happened. The dip buyers came charging back, the semis that got crushed last week ripped, and the relief rally was on.

Quick bit of honesty: I am getting this to you a touch later than planned, which actually works in your favor. Instead of guessing at the week ahead, we already have Monday’s tape in hand, and it is telling us a lot. So here is the plan: we break down what happened last week, what Monday just confirmed, what is still coming in this holiday shortened jobs week, walk the index charts, and then for the paid members we get into the flow, the prints, the watchlist (which already started paying us), and exactly where the book sits right now. Take a seat & let’s dive in.

The Tape: Last Week in Review

Here is the scorecard for the week of June 22:

S&P 500 closed Friday around 7,354, down roughly 2% on the week

Nasdaq Composite closed near 25,298, down about 4.6% on the week and riding a five session losing streak, its first four day skid since February before Friday made it five

Dow closed around 51,876, actually up about 0.6% on the week and printing fresh intraday records along the way

Russell 2000 was the quiet winner again, closing green on the week with small caps catching a real bid

Read those four lines back and the story writes itself. This was not a market falling apart. This was money leaving one room and walking into another. On multiple down days last week, advancing stocks still outnumbered decliners. That is the textbook signature of rotation, not liquidation.

What got hit? Anything with “AI” stapled to it. The semis led the carnage. The SMH chip ETF got smoked roughly 7% in a single Tuesday session as Asian tech cratered overnight, with South Korea’s Kospi tripping a circuit breaker and closing down almost 6%. The catalyst that kept the pressure on all week was a New York Times report that OpenAI is leaning toward pushing its IPO out to 2027, partly because SpaceX has struggled badly since its own June debut and partly because the AI tape has just gotten too choppy. That report did two things: it raised questions about how all this data center spending gets funded if the capital markets window is closing, and it gave every nervous tech holder a reason to hit the bid.

Even good news could not save tech. Micron reported a genuine blowout after the bell Wednesday, adjusted earnings of $25.11 against about $20.78 expected, and the stock ripped 17% on Thursday. And the Nasdaq still closed red Thursday because the money coming out of Apple and Microsoft was bigger than the money chasing Micron. Apple dropped 6% after announcing price hikes on the MacBook and iPad. Microsoft fell over 3% on Xbox price increases, both of them pointing at higher memory costs, which is its own quiet little tell about where the chip cycle is squeezing. Then Friday, Micron itself gave back nearly 7% as traders booked the pop.

Meanwhile, the boring stuff worked. Caterpillar jumped 6% on Thursday. Healthcare, industrials, and financials carried the Dow to records. Eli Lilly soared 7% Friday after the EU backed one of its leukemia therapies. Moderna was the top S&P name Friday on its in vivo CAR-T investor day. Bio-Techne popped 19% on a Merck buyout. The rotation was not subtle.

A couple of macro tailwinds quietly helped the broad market hold. Oil kept falling all week as tankers continued moving through the Strait of Hormuz unimpeded, with Brent sliding back toward pre-war levels near the low $70s. Cheaper oil eased the inflation worry, which matters a lot right now given where the Fed's head is at. And Friday's PCE print came in cooler than feared on the month over month read, which took some of the edge off.

The Headlines

Quick rundown of the stories that set the table over the weekend and ran through Monday’s session, plus the context that still matters going forward:

The Iran ceasefire is back on shaky ground. Over the weekend, President Trump ordered fresh US strikes on Iranian missile and drone sites, saying Tehran violated the cease fire agreement again, and renewed his threats against the regime. Kuwait and Bahrain reported incoming missiles and drones overnight. Here is the tell though: oil did not spike and the market rallied anyway on Monday, because crude is still sliding back toward pre war levels and traders are betting this stays contained. That is a powerful signal of risk appetite, but it is also the kind of complacency that can reprice fast, so keep one eye on crude.

OpenAI’s IPO drama is now a market input. The reporting says Altman was given two options by advisers: wait until 2027 for a trillion dollar valuation, or list sooner at a lower number, and that he called anything under a trillion a nonstarter. Until that resolves, it hangs over the entire AI infrastructure complex, because the whole data center buildout thesis assumes the capital keeps flowing.

The Dow got a facelift, effective today. Alphabet officially joined the Dow Jones Industrial Average this morning, replacing Verizon, and celebrated its first day as a member by climbing more than 4% while Verizon dropped over 5%. It makes the “boring” Dow a little more tech sensitive going forward, even as it prints records.

The Fed independence fight got a ruling. The Supreme Court ruled Monday, 5 to 4, that President Trump cannot remove Fed Governor Lisa Cook for now, keeping her in her seat while her lawsuit plays out. With Kevin Warsh already in the chair and an actual rate hike on the table this cycle, anything touching Fed independence is worth tracking, because it feeds straight into how the bond market prices risk.

M&A and corporate action is picking up. ON Semiconductor agreed to buy Synaptics. Merck is buying Bio-Techne for $11.3 billion. And the one that matters for a lot of you: CrowdStrike’s 4 for 1 stock split takes effect Thursday, July 2. If you are holding or watching CRWD, your share count and strike math are about to change.

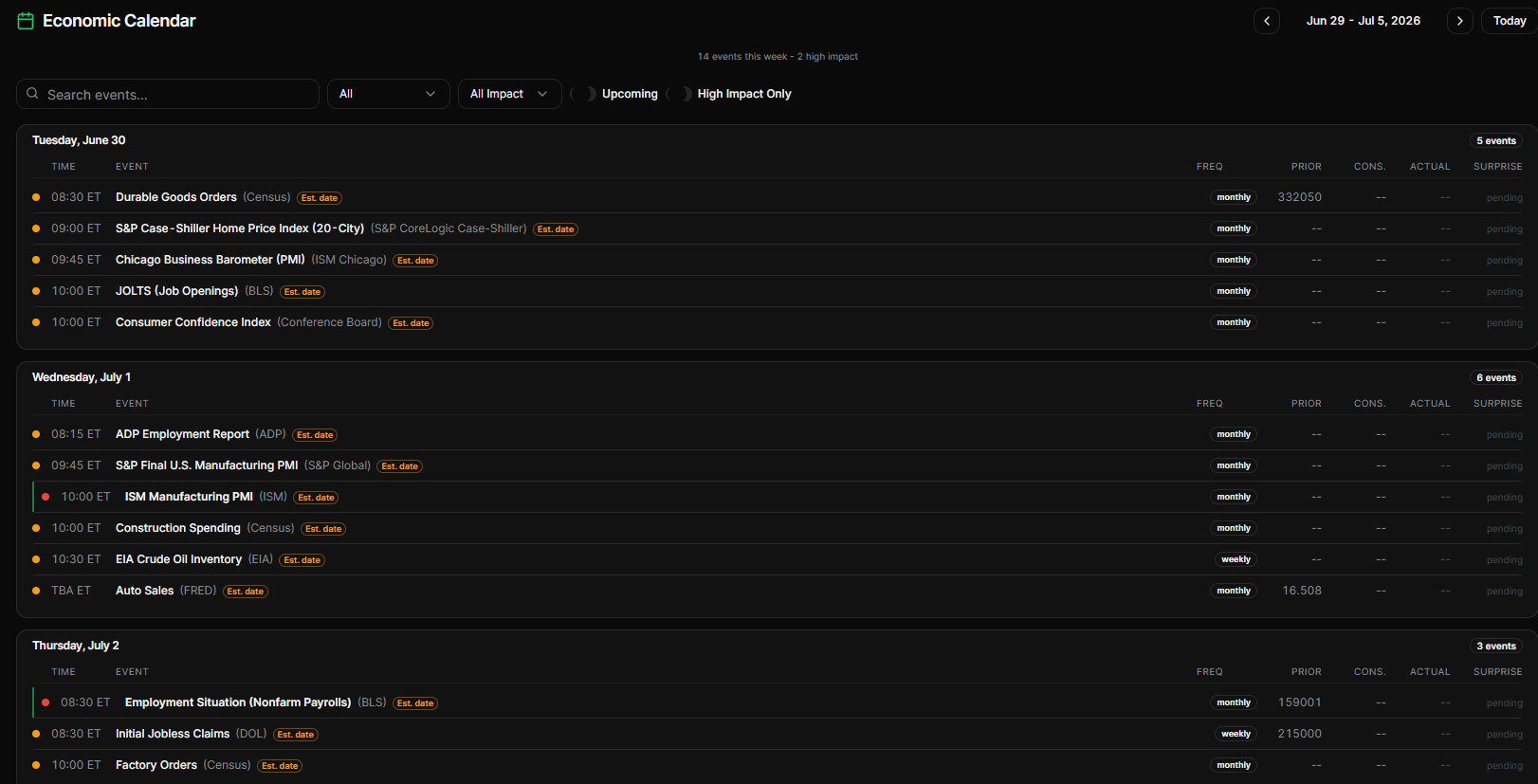

What’s Coming: A Holiday Shortened Jobs Week

This is a front loaded, data heavy week that ends early. Markets are closed Friday, July 3 for Independence Day, which means everything gets crammed into four sessions and the big number lands a day earlier than usual.

Here is the calendar that matters:

The whole week builds to Thursday’s jobs report. Consensus is sitting around 172,000 jobs for June, with the unemployment rate expected to hold near 4.3%. Here is why the framing matters more than usual this cycle: the conversation around the Fed has flipped. We spent the first part of the year debating how many cuts we would get. Now, with Kevin Warsh running the Fed and a Bank of America note last week openly floating the risk of rate hikes, the market is pricing the FOMC to hold in July and watching every data point for which direction the next move breaks. A hot jobs number plus any stickiness in wages feeds the hike narrative and pressures the long end. A soft number cools it off and is probably a green light for the small cap and rotation trade that is already working.

So the setup into Thursday is asymmetric in an interesting way. The part of the market that has been leading (small caps, industrials, financials, value) wants to see the economy stay resilient without reigniting the inflation fight. That is a needle to thread.

One more on the radar just past the week: Penguin Solutions (PENG) reports Q3 after the close on Tuesday, July 7. More on that name below, but mark it.

The Charts: SPY, QQQ, IWM, DJI

Let’s walk them. The four charts together tell the rotation story better than I ever could in words. The dip got bought.

(SPY)

SPY closed Monday at 741, a 1.65% pop on the week candle, and we are right back up near the all time high at 749.53. The pullback from the highs found buyers in a hurry, the weekly candle is green (of course), and price is sitting comfortably above every weekly moving average. Immediate support is the shelf at 740.86 to 739.56 we are basically resting on, then a real gap down to 707.39, and below that the 689 to 684 zone where the rising mid term averages live. As long as SPY holds the 740 shelf, the path of least resistance is a retest of 749 and then blue sky above it. This is a strong chart, don’t overthink it.

(QQQ)

And here is the redemption arc. Last week I flagged the 706 to 695 band as the battleground, the zone that decided whether "rotation" stayed the right word. Here is what the buyers did with it: they did not even wait for the deep end. QQQ showed strength this week at 705.17, right at the top of that zone, held it cold, and ripped back to 724.08, a 2.49% gain on the daily candle, reclaiming the 714.78 and 722.03 levels in a single move. The 695.93 support I had marked underneath never even got tested, which tells you how aggressive the bid was. So now the 705 to 706 shelf is the floor that held, 722 to 724 is the zone we are punching back through, and the recent high up near 740 is the target if this follow through sticks. Lose 714 and then that 705 shelf and we are back to chop, but for now the leader did precisely what a leader is supposed to do off support. Beautiful.

(IWM)

This one has quietly been the tell. While SPY and QQQ were getting sold last week, the Russell showed real relative strength and held green, exactly the kind of small cap leadership you want to see if the rotation is the real deal. This week it is taking a well earned breather while tech plays catch up, and that is perfectly fine. IWM closed 298.97, basically flat on the day (down a hair), still pinned right under the 300 round number that has been the ceiling. The chart is still pristine - price above all of its moving averages (the 8 and 21 week sit at 288.56 and 272.97), riding the rising channel, no damage done at all. This is healthy consolidation at the highs, not weakness. The Russell is coiled right under 300, and if Thursday’s jobs number cooperates, this is the chart that continues to break out. It led when tech was red and it is resting now that tech has bounced. Watch for it to take the baton back.

(DJI)

The Dow does not stop. DJI closed Monday at 52,188, a fresh record, up 0.59% on the week and printing new highs inside a clean rising channel. Above every moving average, with the first real support down at the 50,798 shelf, then 49,224 and the 48,756 breakout level beneath that. Industrials, financials, and healthcare keep doing the heavy lifting, and with Alphabet now in the index there is a little more tech torque under the hood too. Nothing bearish to say here. The trend is your friend until it bends, and it is not bending.

Bottom line on the indices: all four are constructive, and three of them (SPY pressing the highs, QQQ via the bounce, and the record setting Dow) are flashing real strength while the Russell coils under 300. QQQ holding its support up around the 705 to 706 shelf, without ever needing the deeper 695 level, was the whole ballgame, which is exactly why Monday was a buy the dip session and not a breakdown. The semis ripped right along with it (the SMH chip ETF swung from down roughly 3% intraday to up over 3%, with Astera Labs, Applied Materials, and KLA each running more than 11%). The thesis we built last week, that this tape wants to rotate, not break, just got confirmed in real time. Now the only question that matters is whether the bounce has the legs to push through into Thursday’s jobs print, or whether we chop sideways up here until the number drops.

Volux: Something New Is Coming

Quick one before we roll into the members section, because I am genuinely fired up about this.

We have been heads down building Volux, and we just locked in a TradingView partnership that I think is going to change how a lot of you trade alongside this letter. The short version: Volux subscribers are going to get full access to the complete suite of indicators and functions, the same toolset I am using to mark up these index charts every week, integrated so you are not stitching things together across five tabs anymore. Flow, levels, and the charting all in one place among many other tools at your disposal.

I am not going to spoil the whole thing yet. What I will say is to keep your eyes on this space heading into July. That is all I am saying.

Everything below is for paid subscribers. Thanks for being here. This is where the real work is.