Weekly Juice

Feb 17 - Feb 20

Markets are closed today for Presidents' Day. It's a shortened but loaded week. Today’s letter is free for everybody so I hope you enjoy just a light read with some key information and things to watch for this week.

The Big Picture

Last week was ugly. The S&P 500 closed Friday at ~6,836 after flirting with its 100-day moving average, a level it hasn’t settled below in nearly a year. The Nasdaq posted back-to-back weekly losses. But here’s what matters: the selling wasn’t about fundamentals. It was about fear.

AI disruption anxiety spread like wildfire last week. What started as a software selloff turned into a full-blown rotation out of anything Wall Street decided could be “disrupted” / trucking stocks (C.H. Robinson and RXO each dropped 20%+), real estate (CBRE -16%), wealth management (Schwab -10%), even media names like Netflix. JPMorgan’s trading desk summed it up perfectly:

“The market is struggling to understand the full scope of what AI can do.”

Meanwhile, underneath the noise, the macro picture actually improved. January CPI came in at +2.4% year-over-year, the lowest since May 2021. Core CPI was in line. Treasury yields dropped across the curve, with the 10-year falling to 4.05%. This should have been bullish. It wasn’t. That disconnect tells you something about the current market psychology: fear is driving the tape, not data.

The Fed rate cut timeline shifted after a strong jobs report / March probability dropped to just 10%, June is now the base case at ~85%. Kevin Warsh, nominated to replace Powell in May, has adopted a more pragmatic tone, suggesting the Fed should “look through” tariff-driven price spikes. That’s a dovish tilt from a known hawk.

Earnings season is 74% complete. 76% of S&P 500 companies have beaten on the bottom line, with blended EPS growth tracking at +13.2% - a fifth straight quarter of double-digit gains. The fundamentals are fine. The question is whether sentiment catches up.

This Week’s Earnings Calendar / The Names That Matter

This is one of the most consequential earnings weeks of the season. Here’s your day-by-day breakdown of the reports that could move markets:

Tuesday

PANW: Cybersecurity bellwether reporting after close. Stock is down 10%+ from 50-day MA. Watch ARR growth, billings guidance, and commentary on the Chronosphere + potential CyberArk acquisition closings. DA Davidson cut PT to $210 but kept Buy. A guidance raise could spark a mean-reversion rally.

CEG: Power generation trade still alive. Nuclear/AI data center narrative is the story here. Watch for updated guidance on power purchase agreements and capacity expansion.

MDT: Healthcare bellwether. Steady but watch for any medical device AI integration commentary.

CDNS: EDA/chip design software. In the AI disruption crosshairs / could bounce or get hit further depending on guidance.

ET: MLP/energy infrastructure play. Dividend and distribution guidance is the focus.

Wednesday

CVNA: THE event of the week. See deep dive below. Binary outcome - short squeeze or breakdown. Options pricing a ~15.5% move. Reporting after close.

BKNG: Travel demand bellwether. After Airbnb's upbeat outlook, expectations are elevated. Watch international booking trends and AI-powered travel tool commentary.

DASH: Delivery/gig economy. After DraftKings' guidance disaster (-17%), the consumer discretionary/platform space is under scrutiny.

EBAY: E-commerce turnaround story. AI-powered listing tools driving engagement.

ADI: Semis. Industrial and automotive end-market demand signals matter here.

OXY: Energy. Watch production guidance and Permian Basin commentary.

Thursday

WMT: Consumer spending bellwether #1. Last quarter was strong (+5.9% YoY revenue, e-commerce +27%). Guidance for FY27 is the focus / any tariff impact commentary will move the tape broadly. This is the single most important macro read of the week.

BABA: China + AI narrative. DeepSeek reverberations continue. Watch cloud revenue growth and AI infrastructure spend.

DE: Agriculture/industrial cycle read. Tariff impact on farming equipment demand.

NEM: Gold miner. Gold at $5,035/oz / watch production costs and reserve updates.

SO: Utility/power. AI data center power demand narrative.

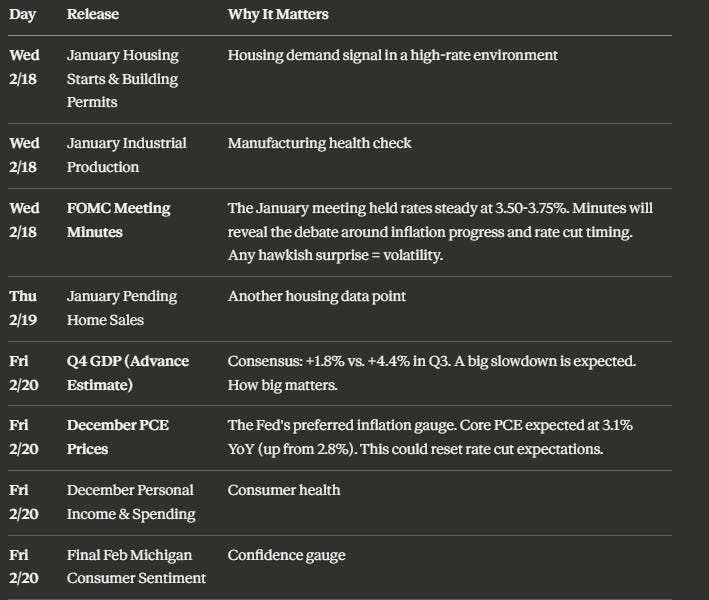

Good bit of Economic Data this week to focus on as well…

Key Points:

The FOMC minutes on Wednesday and PCE data on Friday are the two macro landmines this week. If PCE comes in hot at 3.1%+ on the core, it pushes the June cut narrative into question and could trigger another leg down in growth stocks. If it’s softer, we get relief.

I want to talk about Carvana as the asset has been under heavy selling pressure as of late with a ton of negative press including short reports, and growing narrative of delinquencies etc. so let’s dive in shall we?

The Binary Bet of the Week…

The Setup: CVNA hit an all-time high of $486.89 on January 22. Since then, it’s crashed ~29% to ~$367 after Gotham City Research published a devastating short report alleging $1B+ in overstated earnings through undisclosed related-party transactions with DriveTime/Bridgecrest (both controlled by CEO’s father). Multiple law firms (Block & Leviton, Pomerantz, Bragar Eagel) have opened securities fraud investigations. Insider selling has been massive, the CEO has dumped over $1.4 billion in shares since April 2024.

What the Bulls Need: A clean 10-K filing on time. Beat-and-raise on Q4 numbers (consensus: $1.10 EPS, ~$5.2B revenue). Explicit management commentary addressing the Gotham allegations with data. If all three happen, shorts (11.4% SI) get squeezed and the stock could rip 15-20%+ in a single session.

What the Bears Need: Any delay in the 10-K filing. Auditor (Grant Thornton) issues or qualifications. Weak Q4 numbers or soft guidance. If the 10-K doesn’t file or the auditor flags anything, this stock could revisit sub-$200.

The Flow: Bearish options flow has been building for two weeks. Options are pricing a ~15.5% move. This is a pure event-driven, binary trade. Not for the faint of heart.

Carvana operates in the online used vehicle retail industry, running a vertically integrated e-commerce platform for buying, selling, financing, and delivering used cars across the U.S. In Q3 2025, the company sold a record 155,941 retail units (up 44% YoY) and posted record revenue of $5.65B (up 55% YoY). Yahoo Finance

The company also operates wholesale auction sites through its ADESA acquisition. Primary competitors include KMX (CarMax), LAD (Lithia Motors), AN (AutoNation), CARG (CarGurus), and ACVA (ACV Auctions). Analysts project EPS to climb ~428% YoY to $5.39 in FY2025 and grow another 37% to $7.39 in FY2026. Yahoo Finance

Carvana's competitive moat lies in its technology-driven, asset-light digital platform, proprietary logistics/reconditioning network, and data advantages that traditional dealerships cannot replicate at scale. The company was added to the S&P 500 in December 2025, a massive validation event. What makes CVNA unique is the dramatic turnaround, it rose over 12,000% from 2022 lows near $3.56 to highs of ~$486. However, a short-seller report from Gotham City Research in January 2026 alleging $1B+ in overstated earnings has created significant near-term uncertainty ahead of the February 18 earnings release.

The used auto retail sector has been weak overall, pressured by higher interest rates impacting consumer affordability. However, CVNA has been the worst performer in the group over the last month due to idiosyncratic risk (Gotham report). Over 12 months, CVNA still dramatically outperforms all peers (+93% vs KMX -52%).

Analyst Price Targets for the most part still reside higher, ranging from $460 - $530 with some even calling the sell-off as a buying opportunity (where I sit as well).

TLDR Bull / Bear:

BULL CASE:

If Q4 earnings beat and 10-K files clean on Feb 18, shorts get squeezed hard (11.4% short interest)

JPMorgan expects “solid beat and raise” / consensus Q4 EPS of $1.10 (+96% YoY)

Used car demand tailwind as new car prices stay elevated (~$50K avg)

S&P 500 inclusion ensures ongoing passive fund demand

Consensus PT of ~$462-498 implies 25-35% upside from current levels

BEAR CASE:

If 10-K is delayed or auditor raises concerns, the stock could revisit sub-$200

Massive insider selling is a red flag that’s hard to ignore

Gotham City allegations on related-party transactions are serious and not yet fully addressed

Valuation still rich at ~78x PE despite pullback

Multiple securities fraud investigations now open

Operating cash flow declining (slipped to $606M from $858M YoY through Q3)

In summary, this week we have earnings, macro data, and Fed signals all converging. The markets are nervous but not quite broken. With the S&P stuck in a range this week’s data could determine which side breaks first. Our watchlist this week is considerably lengthy between Friday’s piece and today’s piece discussing the upcoming earnings & econ data. While I don’t anticipate trading everything we have discussed, it’s still important to watch them for reactions as a gauge on future bets / money flows from a sector stance.

Thanks for tuning in & supporting the Unusual Flow substack. As always, likes and comments are greatly appreciated as well as shares / restacks. See you guys tomorrow for the flows and I hope you guys enjoyed the long weekend.

Cheers,

Jersace