Jersace's Juice List - Vol. 3

"Is the Juice Worth the Squeeze?" In Short, Yes.

Hello,

What a year it has been.

Welcome back to the Juice List! To those who have followed me for quite some time or chat with me regularly, you know this list has become something of a tradition. Vol. 1 helped set the stage back in January 2024, and Vol. 2 published at the tail end of 2024 absolutely delivered. Now, as we close out another incredible year, it’s time for Vol. 3.

The 2025 Juice List wasn’t just about picking stocks that would go up. It was about identifying a structural shift so profound that it would revalue entire sectors. 2025 was a phenomenal year for markets.

The big themes of 2025 were clear: AI infrastructure remained king, nuclear energy emerged as a legitimate growth story, memory and storage stocks exploded, and the “picks and shovels” trade expanded beyond semiconductors into power generation and grid infrastructure. Gold hit all-time highs above $4,500, silver broke $70, and commodities broadly rallied as inflation concerns persisted into the first half before easing.

The remarkable thing isn’t that these stocks from Vol. 2 went up as much as they did. The remarkable thing is how few people understood why they went up. Most investors saw “AI stocks” and chased semiconductor names. The real trade was understanding that silicon without electricity is worthless, and that we’d created an energy constraint that would take a decade to solve.

As we position for 2026, I want to be crystal clear about what we’re doing and why. This isn’t a momentum portfolio. This isn’t a collection of “AI plays” because AI is trendy. This is a calculated bet on the largest coordinated infrastructure build-out since the interstate highway system of the 1950s (in other words, the best thing since sliced bread), and we’re positioning ourselves in front of every bottleneck, every capacity constraint, and every material shortage that build-out will create.

Now let's see how the Vol. 2 basket performed and get into what I'm watching for 2026.

Vol. 2 Performance Recap

The Vol. 2 list published in late December 2024 absolutely crushed it. Let me break down how each name performed throughout 2025:

The Big Winners

GOOGL (+66% YTD): The undisputed champion of the basket. The Willow quantum chip announcement we highlighted delivered, Google Cloud continued to dominate, and Waymo expanded its robotaxi footprint. Alphabet emerged as one of the Magnificent Seven’s top performers alongside NVIDIA.

JOBY (+75% YTD): The eVTOL thesis played out beautifully. Joby entered TIA testing (the final stage of FAA certification), acquired Blade’s passenger business, and secured major international deals in Dubai and Saudi Arabia. The company is positioned to potentially launch commercial operations in 2026.

UBER (+51% YTD): Our risk/reward play from Vol. 2 nailed it. Goldman Sachs’s $97 target was hit and exceeded as UBER reached all-time highs above $100 in September 2025. The autonomous vehicle concerns we noted ultimately didn’t derail the stock - Uber partnered with multiple robotaxi companies instead of being disrupted by them.

GEV/VST/CEG (Energy Trifecta): These names crushed it. GEV nearly tripled since its April 2024 IPO. CEG gained roughly 45-60% as Meta, Amazon, and Google signed massive nuclear power deals. The AI power demand thesis we outlined became THE story of 2025.

TLN (Talen Energy): Another nuclear winner. The Amazon partnership we highlighted expanded to 1,920 megawatts through 2042. Earnings projections soared, with 2026 EPS expected to jump over 300%.

HIMS (+36% YTD, hit $73 ATH): The GLP-1 weight loss play delivered early in the year, with shares surging to all-time highs near $73 in February before pulling back. Volatile but profitable for those who caught the move.

TSLA (+18% YTD): Solid gains, though not the explosive move some hoped for. The robotaxi narrative continued building, and the Musk-Trump relationship remained a tailwind.

IONQ: Hit all-time highs above $84 in October 2025 during the quantum computing frenzy, though it’s pulled back since. Those who caught the momentum play banked serious gains.

The Misses

LCID (-65% YTD): The speculative turnaround play didn’t work out. Production scalability issues persisted, and the EV market remained brutally competitive. Risk/reward cuts both ways.

GTLB (-15% YTD): Underperformed despite the DevOps theme. Microsoft’s GitHub integration and broader software compression hurt.

ACHR: More volatile than JOBY, with execution concerns emerging late in the year. Still up significantly from 2023 lows but lagging its peer.

AUR (-38% YTD): This one was interesting because while it didn’t perform well throughout the year, we actually booked a gain on this for over 70% within the first two months of the year.

Each of these names had their moment of green and if executed the trade perfectly, you wouldn’t own any of these at the moment unless you’re still interested in the previous thesis at a lower entry.

The Verdict

Overall, the Vol. 2 basket significantly outperformed the S&P 500’s ~17% return. The energy and autonomous mobility themes we identified were spot-on. Even accounting for the LCID and GTLB misses, a diversified allocation across these names would have generated strong alpha. The juice was absolutely worth the squeeze.

The Broader Market

The S&P 500 returned approximately 17-19%, marking its third consecutive year of double-digit gains. The Nasdaq Composite climbed over 21%, and the Dow added around 14%. We came within striking distance of the historic 7,000 milestone on the S&P 500, hitting an all-time intraday high of 6,945 during the Christmas rally. The market proved resilient, muscling past the April tariff chaos, rate cut speculation, and concerns about an AI bubble bursting.

The Copper Supercycle

I want to spend time on copper because I believe this is the single most underappreciated macro trade for the next three to five years.

Copper demand from AI data centers alone will grow 6x by 2050 according to BHP’s research division, from around half a million tonnes annually today to approximately three million tonnes by mid-century. But here’s the key insight: that growth won’t be linear. It will be front-loaded into the next five years as the massive data center construction boom happens now, not in 2045.

Here’s what makes copper different from other commodities. When you’re building a data center, copper represents less than half of 1% of total project costs. Developers are completely price insensitive. If copper goes from $4 to $6 per pound, it doesn’t change anyone’s decision to build. This inelastic demand in a supply-constrained market is the recipe for explosive price appreciation.

On the supply side, the picture is bleak. The US averages 29 years to permit and build a copper mine. Chile’s state miner Codelco faces stagnation. First Quantum’s Cobre Panama mine closure removed substantial supply. BHP and Freeport-McMoRan both face rising capital requirements for new production. The industry has been underinvesting for fifteen years, and you can’t fix a decade of underinvestment overnight.

Wood Mackenzie warns that insufficient mine investment could drive sustained shortages and price volatility, with demand potentially surging 24% to 42.7 tonnes per annum by 2035. Goldman Sachs slashed its supply forecasts, now projecting deficits of 160K tonnes in 2025 and 200K tonnes in 2026 even before accounting for recent mining disasters at major facilities.

The investment playbook here is straightforward. We want to own copper producers with low all-in sustaining costs, mines in politically stable jurisdictions, and near-term production growth. We want to avoid development-stage stories with 5+ year timelines because we’re trying to capture the 2026-2028 price spike, not the 2030s. And we want to complement direct mining exposure with copper-intensive infrastructure plays like utilities and cable manufacturers that will benefit from higher throughput volumes even if margins compress slightly. Moving on…

The 2026 Juice List

Before we dive into the list, I’d like to point out that in the past two weeks, I have nearly re-done the entire letter. A few ideas you will find missing as I have already mentioned them in chat and others on hold for the time being with the intention of writing them up in another letter in its entirety focusing on the memory/data storage angle paired with batteries. I was taking the angle of a full blown weighted portfolio structured letter here, however switched gears back into flat-out idea generation built for investing & trading alike.

Now let’s dive into what I’m watching for 2026. The themes have evolved - AI infrastructure is entering its “maturity phase,” healthcare is setting up for a rebound, and the power generation trade has legs left to run. Here are my picks across various sectors and themes:

Theme 1: AI Power Infrastructure: The Trade That Keeps Giving

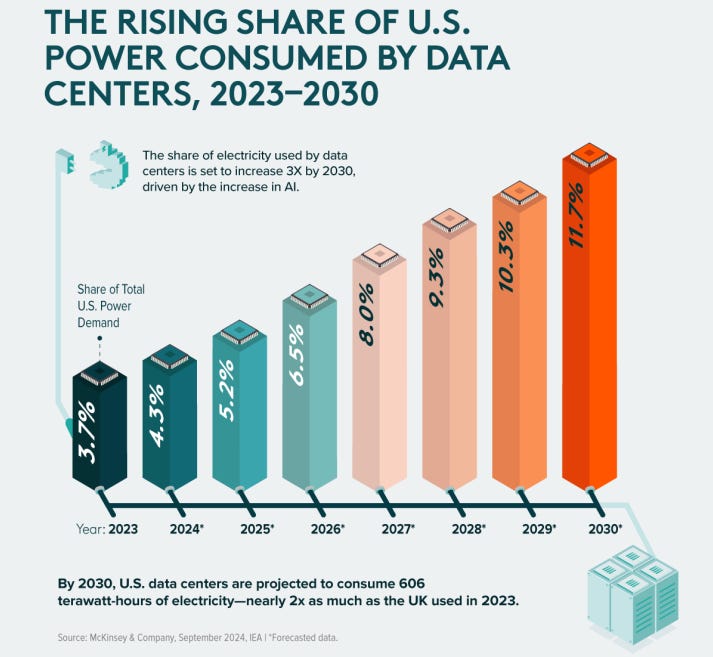

McKinsey estimates global AI-powered data center infrastructure capex will reach $7 trillion by 2030. U.S. data center electricity demand is expected to climb from 19 GW (2023) to 35 GW (2030). This isn’t slowing down - it’s accelerating. The infrastructure buildout is only 20% complete according to Morgan Stanley.

CEG (Constellation Energy)

The undisputed heavyweight champion of nuclear power. CEG is the largest nuclear operator in the U.S. with 20-year power purchase agreements now signed with Meta, Microsoft, and others. The Calpine acquisition for $26.6 billion adds natural gas and geothermal assets, making this a diversified clean energy powerhouse.

The Technical Setup: Trading about 8% off all-time highs after retaking the 50-day moving average. Expected earnings growth of 22-26% in 2026. Trades at 29.6X forward earnings - a 20% discount to its highs.

The Catalyst: Trump administration’s four executive orders aimed at expanding domestic nuclear capacity. The regulatory tailwind is real.

GEV (GE Vernova)

Still my favorite energy play. GEV customers generate roughly 25% of all electricity in the world via its installed base. The company provides exposure to nuclear, natural gas, small modular reactors (SMRs), grid solutions, and electrification software. Revenue expected to reach $45 billion by 2028 with $14 billion in cumulative free cash flow. This screams $1000/share.

Stock has increased over 500% since April 2024 IPO. Recently announced $6 billion buyback program and its first dividend. Projected 237% earnings growth in 2025, setting up for continued momentum.

The Catalyst: Electrification backlog expected to double in the next 3 years. Every AI hyperscaler is a potential customer.

TLN (Talen Energy)

Another big winner from 2025. The Amazon-backed nuclear play. TLN has a deal to provide AWS with 1,920 megawatts of carbon-free nuclear power through 2042. Recently expanded by acquiring natural gas plants, boosting generation capacity by 50%.

The Technical Setup: 12 of 13 analysts have Strong Buy ratings. EPS projected to jump 300%+ in 2026 on 75% revenue growth.

The Catalyst: Potential for additional hyperscaler deals. The data center demand pipeline is massive.

NEE (NextEra Energy)

The renewable and nuclear utility giant. NEE has crushed the S&P over the past 25 years (810% vs 460%) yet has traded essentially ‘flat’ for the last 4 years. Recently partnered with Google to restart the Duane Arnold nuclear facility in Iowa, plus signed multiple GW-scale solar and storage deals with Meta.

The Technical Setup: Trading 15% below all-time highs after being rejected at resistance multiple times since 2021. Rate cuts make the dividend yield more attractive. This could be the year it finally breaks out.

Theme 2: AI Infrastructure: Builders

NVDA (Nvidia)

The undisputed king. NVDA is up 42% YTD and remains the second-best performing Mag 7 stock behind only Alphabet. But here’s the thing, after two years of triple-digit returns, the “slowdown” narrative created a buying opportunity that Wall Street is now reversing hard on.

The numbers are staggering: Nvidia has a $500 billion AI chip order book for 2025 and 2026 combined, and Q4 fiscal 2026 revenue is expected to hit $65.6 billion with EPS growth of 69% YoY. Data center is 90% of revenue now and accelerating. Q3 showed 62.5% revenue growth, up from 56% in Q2. When was the last time you saw growth accelerate at this scale?

The 2026 catalyst is clear: the Vera Rubin platform launches, and if it delivers the promised performance uplift, it destroys any remaining doubt about Nvidia’s supremacy. Jensen stays several steps ahead. Cantor Fitzgerald calls NVDA their “top pick” with Tigress raising their target to $350. Mean analyst target sits at $261 with a Street-high of $433.

The Juice: This is still the AI trade. 92% GPU market share. CUDA lock-in. The Groq acquisition adds inference capabilities, and China H200 exports resume in 2026. Premium valuation, but premium asset. You’re not buying a chip company, you’re buying the backbone of the AI revolution essentially BUILDING the ecosystem we all invest in daily.

Risk: Valuation remains elevated. Any demand stumble or hyperscaler pivot to in-house chips (Google TPUs, Amazon Trainium) creates headline risk. China regulatory overhang persists.

AMZN (Amazon)

The Mag 7 laggard becomes the 2026 value play. AMZN is up a mere 3.6% YTD - the worst-performing Magnificent 7 constituent - while the S&P ripped 18%. That’s a 15-point gap that has Wall Street salivating.

Why the underperformance? Rising competition from Walmart, Temu, and Shein on retail. AWS market share losses to Azure and Google Cloud. Fair concerns. But here’s what the market is missing: AWS reaccelerated to 20% revenue growth in Q3, its fastest clip since 2022.

The setup for 2026 is compelling. Data center deal activity hit a record $61 billion in 2025, and Amazon is spending aggressively to capture it. The company plans to invest $125 billion in capex in 2025, growing further in 2026, with plans to double data center capacity by 2027. Oppenheimer estimates each incremental gigawatt of capacity generates $3 billion in annual revenue.

Six major brokerages - BMO, TD Cowen, Wedbush, Truist, J.P. Morgan, and Evercore ISI - have named Amazon a “top idea” for 2026. Mean price target is $296, representing 30% upside from current levels.

The Juice: At 32x forward P/E versus its 5-year average of 44x, AMZN is statistically cheap for the first time in years. AWS is the profit engine, advertising is a $50B+ business growing 20%+, and Prime continues compounding. The “boring” Mag 7 stock might be the best risk/reward of the bunch.

Risk: Capex-heavy model pressures free cash flow near-term. AI shopping agents could disrupt ad revenue. Retail margins remain razor-thin.

CLS (Celestica)

The networking infrastructure play. Celestica provides rack-scale computing solutions for AI data centers, including parts for Google’s custom ASIC chips (TPUs). Revenue grew 28% in Q3 2025 with expectations of 33-34% growth through 2027.

The Catalyst: Leading provider of Google TPU rack-level solutions. Mass production of liquid-cooled AI rack components begins in 2026.

LITE (Lumentum Holdings)

The optical connectivity play. AI servers require massive optical connections - every GPU needs to connect to every other GPU. Lumentum makes the switches, transceivers, and laser-based optical parts that enable this. Stock surged 372% in 2025.

The Catalyst: As AI systems scale out, optical connections from rack-to-rack and eventually data center-to-data center will be essential. This is infrastructure spending that hasn’t peaked.

Thing about this setup is that it’s basically at highs / gone parabolic recently. So we’re not buying this just yet, but rather keeping it high on the focus list for an opportunity to get into the trade versus adding at highs, which can be favorable at times.

ETN (Eaton Corporation)

The electrical systems play. Eaton supplies the power management and electrical systems that deliver and manage the intensive power needs of data centers. As AI power consumption explodes, Eaton’s solutions become mission-critical.

Theme 3: Healthcare

Healthcare has underperformed for years, but the setup for 2026 is compelling. The sector trades at roughly a 20% discount to the broader market. Q4 2025 saw healthcare deliver notable outperformance - a signal that rotation is beginning. The XLV ETF offers diversified exposure, but I’m highlighting specific names with asymmetric upside.

LLY (Eli Lilly)

The GLP-1 king. Eli Lilly’s Mounjaro/Zepbound franchise continues to dominate the weight loss drug market. The global obesity epidemic isn’t going away, and LLY has the best-in-class drugs.

The Catalyst: Continued production ramp and international expansion. New indications (sleep apnea, cardiovascular) could expand the addressable market significantly.

Tough to buy names / charts like these at highs, so they remain on focus list and nibble significant dips as we did a few weeks back to get our year-ahead position locked in with a nice cushion now and plenty of room for adds.

ISRG (Intuitive Surgical)

The robotic surgery monopoly. Intuitive’s da Vinci systems are the gold standard in surgical robotics. The new Da Vinci 5 platform is driving upgrade cycles, and procedure volumes continue to grow.

The Catalyst: Healthcare is ripe for AI integration. Intuitive is positioned to be the picks-and-shovels play for AI-assisted surgery.

We got long this name back in October prior to their massive earnings beat / reaction off that 430 level marked on the chart. Majority of the position to this point has already been trimmed as we did a good bit of maneuvering in Q4 (for the worse in full transparency) yet this remains one of our few healthcare longs going forward.

VRTX (Vertex Pharmaceuticals)

The gene editing pioneer. Vertex’s CASGEVY (developed with CRISPR Therapeutics) was the first approved CRISPR gene therapy. Their pain franchise and cystic fibrosis dominance provide stable cash flows while the gene therapy pipeline offers explosive upside.

Theme 4: Autonomous Everything: Robotaxis to Humanoids

TSLA (Tesla)

Still on the list. 2026 is the year the robotaxi thesis either validates or doesn’t. The broader rollout is planned, Optimus humanoid robots are ramping production, and the FSD subscription model continues growing. The Musk-government relationship remains a unique catalyst.

Risk/Reward: Trading at 317X P/E is insane by traditional metrics, but this is a bet on execution of multiple moonshot projects. Position size accordingly.

We’ve discussed this name nearly everyday this year so not too much else to touch on out of the ordinary.

JOBY (Joby Aviation)

The eVTOL leader. Joby is positioned to potentially begin commercial air taxi operations in Dubai in 2026, ahead of full FAA certification. The Blade acquisition adds immediate revenue, and the NVIDIA partnership for autonomous flight technology strengthens the moat.

The Catalyst: First commercial passenger flights expected mid-2026. If execution continues, this could be a multi-bagger from current levels.

This one rewarded us for the patience we showed throughout 2024 finally this year. Although, the thesis and narrative remains in tact going forward with even greater catalysts coming to fruition if they remain on track. Key support here against 13 is an attractive entry and we will be entering into this position at 250bps size as a more speculative play.

PATH (UiPath)

The enterprise automation play. UiPath’s robotic process automation (RPA) platform is being enhanced with AI agents. As AI moves from chatbots to actual business process automation, UiPath is positioned to benefit. Trading well below highs with improving fundamentals.

We’ve traded this a few times throughout the year and my thoughts remain the same albeit the volatility that comes with these higher beta / growth names.

RIVN (Rivian)

The EV comeback kid. RIVN is up nearly 70% YTD, with most gains coming in the past two months as the market finally recognized two things: the AI angle and the R2.

In early 2026, Rivian begins production of the R2 - its first model priced under $50,000. This is the Tesla Model 3 moment. The R1T and R1S are $100K+ trucks for wealthy enthusiasts. The R2 opens the door to tens of millions of mainstream buyers. Analysts project $6.9 billion in 2026 revenue with a potential price target of $39 if R2 executes.

The balance sheet is secure: VW’s $5.8 billion joint venture partnership (with $1 billion already delivered) bolsters Rivian’s $7.2 billion cash position. This isn’t a company about to run out of runway.

Rivian just achieved its third consecutive quarter of positive gross profit. The Autonomy & AI Day in December showcased hands-free highway assist and robotaxi ambitions - suddenly RIVN trades as an “AI stock” alongside TSLA.

The Juice: Ford just exited the electric truck market. That’s one less competitor. If R2 delivers, Rivian becomes a real Tesla challenger with actual differentiation (adventure/outdoor brand, commercial vans for Amazon). The stock is still 80% below IPO highs, massive room to recover if execution continues.

Risk: EV demand softening as tax credits expired. R2 launch is make-or-break, any delays crater the stock. Still burning cash quarterly. Execution in scaling to 200K+ units is unproven. I’ve been pounding the table on this name for a couple years now and we’re finally seeing the rewards.

Theme 5: Defense & Space: The New Space Race

RKLB (Rocket Lab)

The small launch leader. Rocket Lab has successfully executed more launches than any other private company besides SpaceX. The Neutron medium-lift rocket in development opens up a massive new addressable market including constellation deployment for DoD.

The Catalyst: Neutron first flight expected in 2026. Space becomes a trillion-dollar industry this decade, and RKLB is the most accessible pure-play.

(This chart is all over the place and trading like an alt-coin on some pumpfun website so we’re just going to disregard this one.)

PLTR (Palantir)

PLTR has transformed from “that government contractor” into the AI enterprise software story.

The AIP (Artificial Intelligence Platform) is the unlock. Palantir cracked the code on enterprise AI deployment. Boot camps that show companies how to integrate AI into operations in days, not months. Government contracts keep stacking (DoD, CIA, NHS), but commercial is where the hockey stick lives. Commercial revenue growth accelerated to 54% YoY in Q3.

S&P 500 inclusion in September 2024 brought index fund flows. The stock ran from $20 to $80+ in 12 months. Absurd? Maybe. But revenue is growing 30%+ with expanding margins, and they’re one of the few software companies that can actually implement AI at scale for enterprises.

The Juice: Palantir is what happens when a company becomes the de facto AI operating system for governments and Fortune 500s simultaneously. Peter Thiel built this for decades. The valuation (200x+ forward earnings) prices in perfection, but if AIP adoption continues its trajectory, the multiple compresses into the growth.

Risk: Valuation is eye-watering by any traditional metric. Government contract timing creates lumpy quarters. Concentration risk with large deals. If AI hype cools, this gets hit first.

ONDS (Ondas Holdings)

The drone wars dark horse. ONDS has surged over 350% in the past year as the market finally woke up to the counter-UAS (unmanned aerial systems) opportunity. This isn’t speculation anymore, it’s execution.

Q3 revenues exploded 500% YoY to $10 million, with a $23 million backlog. Management raised 2025 guidance to at least $36 million and is targeting $110 million for 2026. That’s a 3x growth story if they deliver.

The thesis is straightforward: global demand for counter-drone tech is expected to grow from $2.4 billion in 2024 to over $10.5 billion by 2030, a 27% CAGR. Ondas positioned itself perfectly through acquisitions - American Robotics, Airobotics, Sentrycs, Roboteam - building a “system-of-systems” that detects, tracks, and defeats hostile drones.

The Optimus System achieved world-first FAA Type Certification, and the company holds BVLOS waivers allowing drones to fly over populated areas - something most competitors can’t legally do. NDAA compliance makes them one of the few viable options for U.S. government agencies replacing Chinese drone fleets.

Stifel just initiated with a Buy rating and $13 price target, citing a “generational inflection point in military drone adoption.”

The Juice: Defense budgets are expanding. Drone threats are proliferating (Ukraine proved this). Ondas is building the picks-and-shovels for drone warfare - detection, interception, ground robotics. If they hit the $110M 2026 target, this re-rates violently higher. WAR?!

Risk: Small-cap execution risk is real. Cash burn requires continued financing. Acquisition integration complexity. Stock has already run hard - pullbacks likely.

Theme 6: Banks - AI Efficiency

The thesis is simple but powerful: global banks could cut up to 200,000 jobs by 2030 as AI automates human tasks, with back-office, middle-office, and operations roles most at risk. Annual workforce reductions potentially reaching 3%. Major banks have already reported cost reductions of up to 22% through AI implementation.

This isn’t speculation, it’s happening now. JPMorgan’s Marianne Lake said productivity in areas using AI has risen to around 6%, up from roughly 3% before deployment, with operations roles eventually seeing productivity gains of 40-50%. PwC estimates front-to-back-office AI adoption in banking could drive a 15% improvement in the efficiency ratio.

The big money-center banks are leading this transformation and stand to benefit most from the margin expansion as labor costs compress.

I realize that a few of these names are not exactly “banks” however I am blanketing them in this theme for the sake of consolidation as this letter is growing increasingly long the more I research and look around the market… Apologies, I have let it get away from me at this point but man there are some great setups for the year ahead.

JPM (JPMorgan Chase)

he fortress bank that’s also the AI leader. JPM hit fresh all-time highs at $327.78 and is up approximately 37% in 2025, yet the AI efficiency story is just getting started.

JPMorgan is investing $18 billion in technology for 2025, up from $17 billion in 2024, with a strong emphasis on AI and operational efficiency. The ROI is already materializing: CEO Jamie Dimon stated the bank’s $2 billion annual AI investment is now delivering roughly $2 billion in benefits, a 1:1 payback that will only compound. Around 150,000 of the bank’s employees use internal AI models weekly to summarize reports, conduct research, and analyze contracts.

AI agents are now being used for complex trade settlements and fraud detection, which management estimates could eventually reduce operational headcount by 10% while increasing accuracy. The bank’s efficiency ratio sits in the low 50% range already industry-leading, with room to compress further.

Beyond efficiency, JPM is building the future: Kinexys (formerly Onyx) processes $10 billion in daily wholesale payments on blockchain. The bank launched 24/7 on-chain FX settlement in late 2025.

The Juice: JPM is what happens when the biggest bank also becomes the most technologically advanced. CET1 ratio at 15.2% provides massive capital buffer. They’re using AI to widen the moat, not just cut costs. At roughly 12x forward earnings for the dominant franchise in global banking, this is quality compounding.

Risk: Dimon succession (he’s signaled ~2 years to retirement). Commercial real estate exposure. Rate sensitivity if cuts accelerate. Premium to peers means less margin of safety.

HOOD (Robinhood)

The retail trading king. HOOD was one of the S&P 500’s best performers in 2025 (up 215%+). The company successfully diversified beyond payment for order flow with the Gold Card, prediction markets, and crypto trading. S&P 500 inclusion brought institutional visibility.

The Catalyst: Retail trading volumes remain elevated. Crypto bull market provides additional revenue. International expansion opens new markets.

Honorable Mentions:

COIN

The crypto infrastructure play. If you believe Bitcoin and crypto have another leg up in 2026 (as many macro analysts suggest for monetary hedge purposes), Coinbase is the regulated U.S. on-ramp. Revenue leverage to crypto prices is significant.

GS

If you’re going to invest in something, you should own the leader at the least. Keep it simple. We could dive into this deeper but I’ll save you the trouble, this bank is resilient and continues to resolve higher.

BAC

Bank of America has been incorporating AI into their day to day for years now and is considered an AI adoption leader in the financial sector.

Erica, their AI virtual assistant, has now surpassed 3 billion client interactions, serving nearly 50 million users and averaging 58 million interactions per month. But the real story is internal adoption: 90% of Bank of America's 213,000 employees are actively using Erica for Employees, reducing IT service desk queries by over 50%.

Theme 7: Commodities: Gold, Copper, and the Inflation Hedge

NEM (Newmont Mining)

The gold miner with leverage. Gold hit all-time highs above $4,500 in 2025, and central banks continue accumulating. NEM was a top-5 S&P 500 performer in 2025 (up 184%). If gold continues its bull run, miners provide leveraged exposure.

The Catalyst: Geopolitical uncertainty, inflation concerns, and central bank buying all support gold. Morgan Stanley expects gold to remain strong in 2026.

FCX (Freeport-McMoRan)

The copper play. Copper is essential for electrification, EVs, and data center construction. Supply constraints are real, and demand is accelerating. Morgan Stanley has copper as a top commodity pick for 2026. Aligned with MS, this is my favorite commodity for the year ahead as we have seen Gold/Silver go bonkers as of late and much of 2025.

Speculative Ideas: Higher Risk, Higher Reward

These are lottery tickets. Position size accordingly and be prepared to lose the entire investment.

IONQ / RGTI (Quantum Computing)

The quantum theme caught fire in 2025. IONQ hit $84 at peak hype before pulling back significantly. The technology is still years from practical commercial applications, but the Defense Department sees quantum as a “new Manhattan Project.” These are high-volatility momentum plays — trade the swings, don’t marry the positions.

ACHR (Archer Aviation)

The JOBY alternative. If you missed JOBY’s run, ACHR trades at half the market cap with similar certification timelines. United Airlines partnership for 200 aircraft, Stellantis manufacturing deal, and first revenue expected Q1 2026. Higher risk than JOBY but more upside if execution improves.

OKLO (Oklo Inc)

The small modular reactor pure-play. If nuclear energy is the future of AI power (and the thesis is strong), OKLO is building the next-generation microreactors. Sam Altman is an investor. Extremely speculative but interesting as an asymmetric bet on nuclear’s role in AI infrastructure.

UUUU (Energy Fuels)

We have traded / been long this name for many months now and remain long this name currently. Using the daily chart right now for the emphasis on what it looks like today breaking out above 18. Confirmation here would be outstanding as we look to capture a good bit of upside to kickstart the year. While nuclear / uranium still seems to be a good bit of ways away, the opportunity to catch news tailwinds from gov’t spending seems imminent.

The “What-If?”

Let me address the bear cases directly because understanding what could invalidate our thesis is as important as understanding the bull case.

The AI Bubble Pops

The most obvious risk is that AI proves to be a bubble similar to the dot-com boom, where infrastructure gets built far ahead of actual demand and returns on invested capital disappoint dramatically. If enterprises discover that AI applications don’t deliver sufficient ROI to justify continued spending, the entire theme collapses.

I consider this the highest-probability risk we face. The capital expenditure numbers from hyperscalers are staggering, and there’s legitimate question whether AI monetization can justify the infrastructure investment. Microsoft, Meta, Amazon, and Alphabet collectively plan to spend over two hundred billion dollars in 2026. That capital must generate returns or boards will force retrenchment.

However, several factors provide comfort. First, early AI deployments are showing measurable productivity gains in software development, customer service, and content creation. These aren’t speculative use cases. They’re demonstrating positive returns today. Second, the hyperscalers are not stupid. If demand wasn’t materializing, they’d slow spending. Instead, they’re accelerating. Third, we’re positioned in infrastructure that has value regardless of AI. Power generation, memory, and storage have utility beyond AI workloads.

Geopolitical Shocks

Taiwan remains the most obvious geopolitical flashpoint. A Chinese military action against Taiwan would be catastrophic for semiconductor supply chains.

There’s no perfect hedge available. We could reduce position size, but that means giving up returns in the base case scenario where tensions remain manageable. We could buy put options, but hedging geopolitical tail risks is expensive.

Beyond Taiwan, risks include Middle East conflicts disrupting energy markets, trade wars impacting technology supply chains, and domestic political instability. Any of these could create volatility spikes that test our conviction. The key is maintaining sufficient liquidity to weather temporary dislocations without being forced to liquidate positions at precisely the wrong moment.

Technology Disruption

The technology landscape evolves rapidly. New chip architectures could displace Nvidia. Alternative memory technologies could disrupt DRAM and NAND markets. Breakthrough battery chemistry could obsolete current lithium-ion technology. Software platforms can lose relevance quickly if competitors deliver superior products.

Conclusion

2025 was an incredible year, and Vol. 2’s performance validated the thesis: stay positioned in major themes, don’t chase every meme, and let the compounding work. The energy trade we identified is only getting stronger. The eVTOL play is transitioning from speculation to commercialization. The AI infrastructure buildout has years left to run.

The market is entering 2026 near all-time highs with valuations that aren’t cheap. This isn’t the environment for reckless leverage. But within the market, there are pockets of reasonable value and secular growth that should compound regardless of broader multiple compression. Emphasis on something I have kind of worked around on many of these ideas, save some powder for dips. Many of these names are relatively near highs.

As always, do your own due diligence, position size appropriately, and remember that investing involves risk. Not every pick will work… LCID and GTLB reminded us of that in Vol. 2. The goal is for the basket to outperform, not for every individual name to “moon”.

Thank you all for the incredible support over the years. Here’s to making 2026 even more memorable than the last. The juice is always worth the squeeze when you’re positioned correctly.

Cheers,

Jersace

This investment letter represents my personal views and is provided for informational purposes only. It does not constitute investment advice, and you should not rely on it as the basis for any investment decision. Past performance does not guarantee future results. All investments carry risk, including the potential loss of principal. The positions and strategies described may not be suitable for all investors and should be evaluated in the context of your individual financial circumstances, risk tolerance, and investment objectives. Consult with a qualified financial advisor before making investment decisions.

The juice is loose!

Great stuff here, I will be waiting out the first quarter possibly, to make any big moves, trying to stay nimble due to geopolitical news, looking for pullbacks for good entries. Thank you for the hard work here!